One of the highlights of this year’s Surface Transportation Summit was the impassioned plea from Jacquie Meyers, President of Meyers Transportation Services, for shippers and carriers to collaborate. This is not a new message. In fact, it is a message I have heard many times over the past ten years. The difference was the sincerity with which Jacquie communicated her message, the rationale for the message, the unique issues the transportation industry faces as we enter 2014 and the way her message resonated with the audience. I have had the opportunity to read all of the completed post-Summit surveys that we received this year. Jacquie was repeatedly singled out as one of the most important voices at the event.

Trucking companies are not commodities

As we know, the pendulum swings back and forth over time between shippers and carriers. When the economy is weak, shippers can play one carrier off against another as leverage to reduce rates. When the economy is strong and capacity is tight, carriers hold the upper hand and can push through rate increases.

One of the key messages that Jacquie made is that in recent years, shippers have tended to commoditize carriers. The many shippers that have flooded the market with RFPs have tended to focus on price. As several Summit speakers pointed out, some shippers send their RFPs to forty or fifty or more carriers. Jacquie and others expressed the view that shippers often don’t take into consideration the range in quality from one carrier to another. Quality is reflected in superior on-time service performance, superior customer service, late model equipment, strong safety records, excellent shipment tracking tools and low damage claims.

This is a critical issue that seems to be ignored by some shippers. Since a supply chain is only as strong as its weakest link, the use of low priced carriers can result in customer dissatisfaction and lost sales.

The Future is Uncertain

Shippers and carriers face many uncertainties as the economies of North America slowly begin to recover. Will compliance with the new Hours of Service regulations in the United States raise rates? Will carriers continue to be disciplined in adding equipment to their fleets? Is a capacity crunch on the horizon? Are we about to face a driver shortage? Will the economies of North America continue to gain strength? How will this all play out?

While some shippers believe the so-called driver shortage is a myth promoted by carriers seeking to manipulate shippers into accepting freight rate increases, one in two shippers, according to a recent Inbound Logistics study faced a shortage of capacity during the past year, compared to 45 percent in 2012 and 36 percent in 2011. In other words, the shortage is real and getting worse.

Following the Great Recession that hurt much of the trucking industry, and forced many trucking companies to go out of business or streamline assets to better match available capacity with demand, carriers are slowly rebuilding their fleets. For some, it’s a matter of compliance, investing in more fuel-efficient and cleaner-burning tractor engines; others sense the perfect capacity storm that is emerging as freight volumes accelerate and driver recruitment idles.

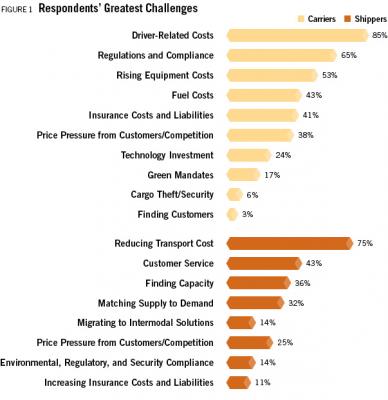

What are the key issues for shippers and carriers?

The chart below reflects the responses from shippers and carriers in the survey. Carrier costs are being pushed up by the challenges in finding and retaining good drivers, compliance with various regulations and other rising costs.

Shippers are facing pressure to reduce transportation costs to maintain the competitiveness of their products while providing good customer service and finding sufficient capacity to deliver their freight.

Now is the Time to Collaborate

Jacquie argued that the best way to address the apparent disconnect is for shippers and carriers to speak with one another, to seek out ways to remove costs and keep freight rates in line. All indicators point to the capacity balance beginning to shift, putting trucking companies in the driver’s seat as shippers begin to search the market and lock up partnerships with preferred carriers.

Carriers are gaining pricing leverage as the economy and freight volumes pick up—and their customers are becoming increasingly aware of this. Many shippers are unsure of how to proceed. Capacity is still soft enough that they have some latitude to negotiate on price, but that window is closing. As shippers become resigned to paying more—and passing along these costs to consumers—their service and reliability expectations will only grow as they demand more value. As Jacquie mentioned, now is the time to talk. It is the time for shippers to select a group of quality core carriers and work through the set of issues that can help keep freight costs in line.